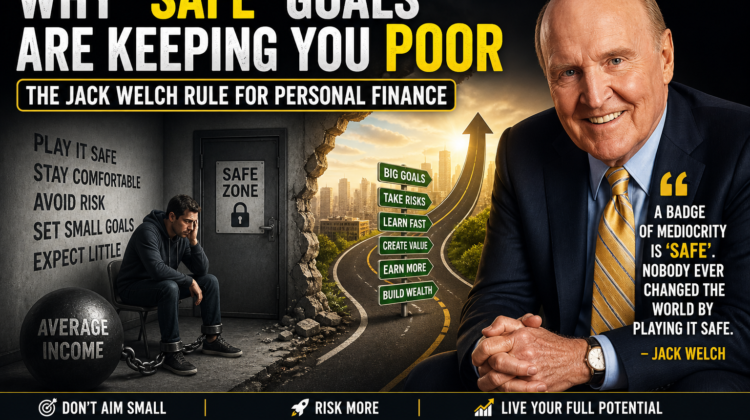

Why “Safe” Goals Are Keeping You Poor: The Jack Welch Rule for Personal Finance

Most people believe that playing it safe is the smartest way to build wealth. Save a little, avoid risks, set realistic goals—and over time, things will fall into place. It sounds logical. It feels comfortable. But here’s the uncomfortable truth: safe goals often lead to average outcomes—and average rarely builds real wealth.

This idea echoes a powerful philosophy popularized by Jack Welch , one of the most influential business leaders of modern times. His approach to growth, performance, and ambition offers a valuable lesson not just for corporations—but for personal finance as well.

Let’s break down why “safe” goals might actually be holding you back—and how thinking bigger can transform your financial future.

The Comfort Trap: Why Safe Feels Right (But Isn’t)

Humans are wired to avoid risk. From an evolutionary perspective, safety equals survival. In finance, this translates into behaviors like:

- Saving small, consistent amounts without scaling up

- Avoiding investments due to fear of loss

- Setting goals that are easily achievable

- Sticking to stable but low-growth income streams

At first glance, these habits seem responsible. But over time, they create a ceiling. You’re not failing—but you’re not advancing meaningfully either.

For example, if your goal is to save ₹5,000 per month, you’ll likely hit it. But will it change your life in 5–10 years? Probably not. Inflation alone will quietly erode much of that progress.

Safe goals keep you busy, but not necessarily wealthy.

The Jack Welch Philosophy: Stretch Goals Win

believed in something radically different: “stretch goals.”

Instead of setting targets you know you can achieve, he encouraged setting goals that feel slightly uncomfortable—even unrealistic at first. Why? Because ambitious goals force you to think differently, act differently, and grow faster.

In business, this meant pushing teams beyond their limits. In personal finance, it means challenging your own financial habits.

For example:

- Instead of saving ₹5,000/month → aim for ₹25,000

- Instead of earning ₹50,000/month → target ₹1 lakh

- Instead of investing cautiously → learn and diversify aggressively

Even if you don’t fully reach these goals, you’ll land far ahead of where a “safe” goal would have taken you.

Safe Goals vs Stretch Goals: The Real Difference

The difference isn’t just in numbers—it’s in behavior.

Safe Goals:

- Require minimal change

- Keep you in your comfort zone

- Lead to predictable, slow growth

- Don’t challenge your mindset

Stretch Goals:

- Force skill development

- Push you to increase income streams

- Encourage smarter investing

- Build confidence and resilience

In short, safe goals maintain your current life. Stretch goals upgrade it.

Income Is the Real Game-Changer

One of the biggest flaws in “safe financial planning” is over-focusing on saving instead of earning.

You can only cut expenses so much. But your income? That has no fixed limit.

If your goal is “save more,” you’ll look for ways to reduce spending. But if your goal is “double my income,” you’ll:

- Learn new skills

- Explore side hustles

- Negotiate better salaries

- Take calculated risks

This shift is powerful.

A person saving 10% of ₹30,000/month struggles to build wealth. But someone earning ₹1 lakh/month—even saving the same percentage—moves much faster.

Stretch goals force you to play the income game, not just the expense game.

Fear of Failure: The Hidden Barrier

Let’s be honest—most people don’t set big goals because they’re afraid of failing.

A safe goal protects your ego. If you achieve it, you feel good. If you don’t, the loss is small.

But ambitious goals come with uncertainty. What if you try and fall short?

Here’s the reality:

Falling short of a big goal is often better than achieving a small one.

If your goal is to earn ₹1 lakh/month and you reach ₹70,000, you’re still ahead. But if your goal was ₹40,000 and you hit it—you’ve limited your growth.

Failure, in this context, isn’t a loss. It’s progress.

The Wealth Gap: Why Average Thinking Costs You

Look around, and you’ll notice a pattern:

- Most people follow “safe” financial advice

- Very few people achieve financial freedom

That’s not a coincidence.

Wealth is rarely built by playing it safe. It’s built by:

- Taking calculated risks

- Investing early and aggressively

- Building multiple income streams

- Thinking long-term and big

Safe thinking keeps you in the middle. And the middle is crowded.

Practical Ways to Apply the Jack Welch Rule

You don’t need to take reckless risks. The goal isn’t chaos—it’s calculated ambition.

Here’s how you can apply stretch thinking in your financial life:

1. Redefine Your Financial Goals

Instead of asking, “What can I comfortably do?”

Ask, “What would truly change my life?”

Set goals that excite and challenge you.

2. Focus on Income Growth

Make increasing your income a priority:

- Learn high-income skills (tech, marketing, finance)

- Start a side hustle

- Invest in personal development

3. Invest Smarter, Not Just Safer

Avoiding investment risk entirely is itself a risk.

Explore:

- Equity markets

- Mutual funds

- Index funds

- Long-term growth assets

Start small, but think big.

4. Build Multiple Income Streams

Relying on one salary is the ultimate “safe trap.”

Stretch your thinking by creating:

- Freelance income

- Passive income (dividends, rent, digital products)

- Business opportunities

5. Upgrade Your Mindset

Your financial life follows your mental limits.

If you believe ₹50,000/month is “enough,” you’ll stop there.

If you believe ₹2 lakh/month is possible, you’ll find a way.

Balance Matters: Smart Risk vs Blind Risk

Let’s be clear—this isn’t about reckless decisions.

Stretch goals should be:

- Ambitious, but not impossible

- Risky, but calculated

- Challenging, but structured

Don’t gamble your savings. Don’t chase shortcuts. Instead, expand your capacity while managing risk intelligently.

Final Thought: Comfort Is Expensive

The biggest cost of safe goals isn’t failure—it’s missed potential.

Every year you play small, you lose time. And in finance, time is your most valuable asset.

The philosophy of teaches us one thing clearly:

Growth doesn’t come from comfort—it comes from challenge.

So ask yourself:

- Are your financial goals truly ambitious?

- Or are they just safe enough to guarantee comfort?

Because in the long run, comfort can be very expensive.

Dare to think bigger. Your future self will thank you.