Rs 3,000 Mutual Fund SIP Vs PPF: Which Can Build Bigger Wealth In 15 Years

When it comes to long-term wealth creation, Indian investors often face a common question: should they invest in a Mutual Fund SIP or choose the safety of a Public Provident Fund (PPF)? Both are popular investment options, both encourage disciplined savings, and both can help create a sizable corpus over time. But if you invest Rs 3,000 every month for 15 years, which option has the potential to generate greater wealth?

The answer depends on several factors such as returns, risk appetite, taxation, and financial goals. Let’s compare both options and understand where your money could grow better over a 15-year journey.

Understanding Mutual Fund SIP

A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly in mutual funds. Instead of investing a lump sum amount, SIP allows investors to contribute monthly and benefit from rupee cost averaging and the power of compounding.

Equity mutual funds, especially diversified funds, have historically delivered annual returns between 10% and 15% over long periods. While returns are not guaranteed and market-linked risks exist, SIPs have become a preferred route for wealth creation among young investors.

Key advantages of SIP:

- Flexible investment amount

- Potentially higher returns

- Power of compounding

- Inflation-beating growth

- Easy to start and stop

However, mutual funds are affected by market fluctuations, meaning returns can vary significantly.

Understanding PPF

The Public Provident Fund (PPF) is one of India’s most trusted government-backed savings schemes. It offers fixed interest rates declared by the government every quarter and comes with sovereign security.

PPF currently has a 15-year lock-in period, making it ideal for long-term investors seeking safety and guaranteed returns.

Benefits of PPF include:

- Government-backed security

- Guaranteed returns

- Tax-free maturity amount

- Eligible for tax deduction under Section 80C

- No market risk

The biggest attraction of PPF is that it falls under EEE status—Exempt, Exempt, Exempt—meaning investment, interest earned, and maturity proceeds are tax-free.

However, returns are comparatively lower than equity-based investments.

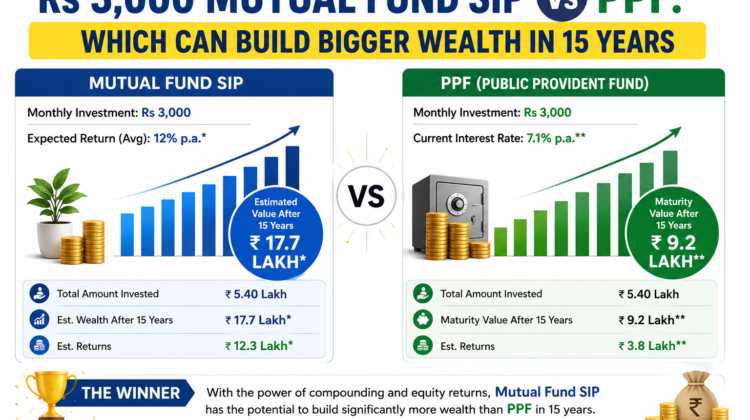

Rs 3,000 Monthly Investment: The 15-Year Wealth Comparison

Let us compare what may happen if you invest Rs 3,000 every month for 15 years.

Scenario 1: Mutual Fund SIP

Monthly investment: Rs 3,000

Investment period: 15 years

Expected annual return: 12%

Total invested amount:

Rs 3,000 × 12 × 15 = Rs 5,40,000

Estimated maturity amount:

Approximately Rs 15 lakh

Estimated wealth generated:

Around Rs 9.6 lakh in gains

This calculation assumes an average annual return of 12%, which many equity mutual funds have delivered over long periods historically.

The magic here lies in compounding. Your money not only earns returns but returns themselves begin generating additional returns over time.

Why SIP Benefits Increase Over Time

In the initial years, growth may appear slow. But as the corpus grows, compounding accelerates wealth creation.

For example:

Years 1–5: Growth appears modest

Years 6–10: Returns start becoming noticeable

Years 11–15: Compounding begins working aggressively

This is why long-term investing often rewards patient investors.

Scenario 2: Public Provident Fund (PPF)

Monthly investment: Rs 3,000

Annual contribution:

Rs 36,000

Investment period: 15 years

Estimated annual interest rate: 7.1%

Total investment:

Rs 5,40,000

Estimated maturity amount:

Approximately Rs 9.5–10 lakh

Estimated gains:

Around Rs 4–4.5 lakh

Since PPF offers fixed returns, growth remains stable and predictable.

There are no market shocks, no sudden declines, and no uncertainty around returns.

SIP Clearly Leads in Wealth Creation

Based on these assumptions:

Mutual Fund SIP corpus: Around Rs 15 lakh

PPF corpus: Around Rs 10 lakh

Difference:

Approximately Rs 5 lakh more wealth through SIP

This gap becomes even wider if market returns exceed expectations.

However, higher returns come with higher risk.

The Risk Factor Matters

One major difference between SIP and PPF is risk.

Mutual Fund SIP:

- Market-linked

- Returns fluctuate

- Potential short-term losses

- Best suited for long-term investors

PPF:

- Government guaranteed

- Stable returns

- No market risk

- Suitable for conservative investors

Many investors panic during market downturns and stop SIP investments midway. This often hurts long-term returns.

Meanwhile, PPF investors enjoy peace of mind due to stable growth.

Your investment choice should match your emotional comfort with risk.

Inflation: The Hidden Wealth Killer

Inflation silently reduces purchasing power over time.

Suppose inflation averages 6% annually.

An investment earning 7% barely stays ahead of inflation.

This is one reason financial experts often recommend equity exposure for long-term goals because equities historically outperform inflation over extended periods.

Mutual fund SIPs may provide better real returns after adjusting for inflation.

PPF protects capital but may struggle to create aggressive wealth growth.

Tax Benefits Comparison

Both SIP and PPF offer tax advantages, but in different ways.

PPF Tax Benefits

- Deduction under Section 80C

- Interest earned is tax-free

- Maturity amount completely tax-free

PPF enjoys complete EEE tax treatment.

SIP Tax Rules

Equity mutual funds are taxed differently.

Long-term capital gains above a certain threshold may attract tax.

Still, even after taxation, SIP returns often remain attractive due to higher growth potential.

Tax efficiency should not be the only deciding factor.

Overall returns and financial goals matter more.

Which Option Is Better For Different Investors?

Choose Mutual Fund SIP if:

- You are comfortable with market fluctuations

- You have long-term goals

- You want potentially higher wealth creation

- You seek inflation-beating returns

Choose PPF if:

- Safety is your top priority

- You dislike market volatility

- You prefer guaranteed returns

- You need tax-free maturity benefits

Can You Combine Both?

Financial planners often suggest avoiding an either-or approach.

Instead of choosing one, many investors combine SIP and PPF.

For example:

Rs 2,000 into SIP

Rs 1,000 into PPF

This strategy balances growth and safety.

The SIP portion targets higher returns, while PPF provides stability and security.

Diversification helps reduce risk while maintaining growth potential.

Final Thoughts

If the goal is pure wealth creation over 15 years, a Rs 3,000 monthly Mutual Fund SIP has the potential to build a significantly larger corpus compared to PPF. With estimated returns around 12%, SIP investments may create nearly Rs 15 lakh versus roughly Rs 10 lakh through PPF.

However, investing is not only about maximizing returns. It is about choosing an option aligned with your goals, risk tolerance, and financial behavior.

SIP may win the race in wealth generation, but PPF wins on stability and safety.

The smartest investment decision is not always the one with the highest return—it is the one you can continue consistently for years without interruption.