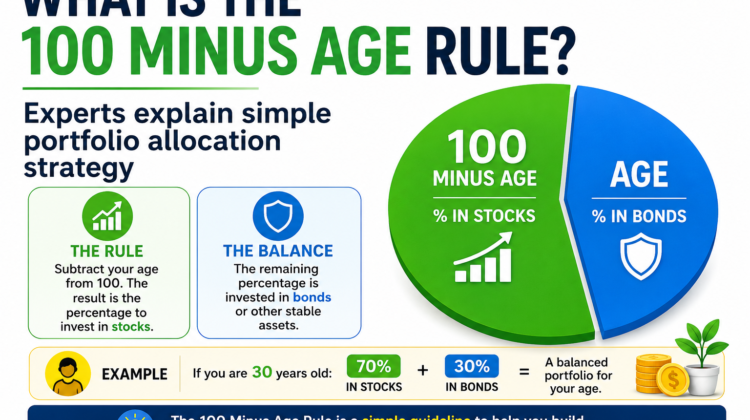

What is the 100 minus age rule? Experts explain simple portfolio allocation strategy

When it comes to investing, one question troubles almost everyone: How much money should go into stocks, and how much should stay in safer investments? New investors often struggle with asset allocation because financial markets can be unpredictable. Put too much money into risky investments and you may face heavy losses. Play too safe, and you might miss out on wealth-building opportunities.

To solve this dilemma, financial experts created a simple formula known as the 100 Minus Age Rule. It’s one of the easiest portfolio allocation strategies and has guided investors for decades. Though simple, it offers a practical framework for balancing risk and growth according to your stage of life.

Let’s understand how this rule works, why investors use it, and whether it still makes sense in today’s financial world.

What Is the 100 Minus Age Rule?

The concept is straightforward:

Subtract your age from 100. The result is the percentage of your portfolio that should be invested in stocks. The remaining amount should be invested in safer assets such as bonds, fixed-income investments, or cash equivalents.

For example:

- If you are 25 years old:

100 – 25 = 75

You should allocate:

- 75% in stocks

- 25% in bonds or safer investments

If you are 40 years old:

100 – 40 = 60

Portfolio allocation:

- 60% stocks

- 40% safer assets

If you are 65 years old:

100 – 65 = 35

Portfolio allocation:

- 35% stocks

- 65% conservative investments

The idea behind this strategy is simple: younger investors have more time to recover from market declines, while older individuals nearing retirement should protect their savings from excessive risk.

Why Age Matters in Investing

Age plays a critical role because investing is deeply connected with time horizon.

A 25-year-old investor may have 30–40 years before retirement. Even if markets fall sharply, they still have decades to recover losses and benefit from future growth.

Meanwhile, a person aged 60 or 65 has less time before retirement. Large losses at that stage can significantly impact financial security because there may not be enough time for the portfolio to recover.

Experts often emphasize that younger investors can afford volatility, while older investors should focus more on capital preservation.

That is exactly the philosophy behind the 100 Minus Age Rule.

The Logic Behind Higher Stock Exposure for Young Investors

Stocks historically generate better long-term returns than safer investments like bonds or savings accounts. However, they also come with greater short-term volatility.

Imagine two investors:

Investor A: Age 25

Investor B: Age 60

Suppose both experience a market crash of 30%.

Investor A still has decades ahead. They can continue investing during market declines and potentially recover.

Investor B may need retirement funds soon and could be forced to withdraw money during a downturn.

This explains why younger individuals typically allocate more money toward growth-oriented assets.

Benefits of the 100 Minus Age Rule

1. Extremely Easy to Understand

You do not need complicated financial software or expert analysis.

Anyone can calculate:

100 – your age

Within seconds, you receive a basic asset allocation guide.

2. Helps Control Emotional Decisions

Many investors panic during market downturns and make impulsive choices.

A predefined allocation strategy creates discipline and reduces emotional investing.

3. Encourages Gradual Risk Reduction

The strategy naturally shifts portfolios toward safety over time.

Instead of making dramatic changes close to retirement, risk decreases gradually.

4. Suitable for Beginners

For new investors overwhelmed by portfolio decisions, this rule offers a practical starting point.

Real-Life Portfolio Examples

Age 30

100 – 30 = 70

Suggested allocation:

- 70% equities

- 30% fixed income

Example portfolio:

- Index funds: 50%

- International stocks: 20%

- Bonds: 20%

- Cash: 10%

Age 45

100 – 45 = 55

Suggested allocation:

- 55% equities

- 45% conservative assets

Example:

- Large-cap stocks: 30%

- Mutual funds: 25%

- Bonds: 30%

- Fixed deposits: 15%

Age 60

100 – 60 = 40

Suggested allocation:

- 40% stocks

- 60% safer assets

Example:

- Dividend stocks: 20%

- Equity funds: 20%

- Bonds and fixed income: 60%

Why Some Experts Prefer the 110 or 120 Minus Age Rule Today

The original 100 Minus Age formula was developed decades ago. Since then, life expectancy has increased significantly.

People are living longer and spending more years in retirement.

Because of this, many financial planners now suggest:

110 Minus Age Rule

or even

120 Minus Age Rule

For example:

Age: 40

Using traditional rule:

100 − 40 = 60% stocks

Using 120 rule:

120 − 40 = 80% stocks

This approach allows investors to maintain more growth exposure for longer periods.

Experts argue that modern retirees may need portfolios to last 25–30 years after retirement, making higher equity exposure necessary.

Important Limitations of the Rule

Although useful, this strategy should not be treated as a universal solution.

Risk Tolerance Differs

Two people of the same age may have completely different comfort levels with risk.

Some investors cannot tolerate sharp market declines.

Others remain comfortable even during volatility.

Personality matters.

Income Stability Matters

Someone with a stable government job may tolerate more investment risk.

Self-employed individuals or people with uncertain income may prefer greater safety.

Financial Goals Are Different

An investor saving aggressively for wealth creation might choose more equities.

Someone approaching retirement may prioritize income and stability.

Existing Assets Matter

Real estate holdings, business ownership, emergency savings, and pensions can influence asset allocation decisions.

Age alone should not determine everything.

Expert View: Use It as a Starting Point, Not a Final Formula

Many financial advisors view the 100 Minus Age Rule as a guideline rather than a strict rulebook.

It provides a useful foundation but should be adjusted based on:

- Risk tolerance

- Retirement goals

- Income stability

- Family responsibilities

- Financial obligations

- Market conditions

Professional portfolio planning often involves a more personalized approach.

Final Thoughts

The 100 Minus Age Rule remains one of the most popular and beginner-friendly investing strategies because of its simplicity. It gives investors a quick way to think about balancing growth and safety throughout life.

For younger investors, it encourages taking advantage of long-term market opportunities. For older individuals, it gradually reduces exposure to risk and focuses on preserving wealth.

Still, investing is not one-size-fits-all. Financial goals, personal circumstances, and risk appetite matter just as much as age.

Think of the 100 Minus Age Rule as a roadmap—not the final destination. It can point you in the right direction, but your personal financial journey should determine the exact route you take.